2021 market forecast: the recovery is gathering pace, but we still have a long way to go

July 22, 2021

The release of Black Widow was a landmark moment for the movie business. The first theatrical release in Phase Four of the Marvel Cinematic Universe delivered the biggest opening weekend since December, 2019, but also ushered in a new business model for a tentpole release by generating $60 million in sales for the Disney+ streaming platform. There’s no way of hiding the fact that Disney has shown that a day-and-date release for a film like this makes sense for the studio, at least while theatrical box office earnings are still depressed due to the pandemic. What that means for the long-term future of the theatrical business is hard to predict.

In the medium term though, recovery at the domestic box office looks like it will continue largely as expected. Our model’s prediction for the 2021 market stands at $5.8 billion today, which is down slightly from last month’s predicted $5.9 billion, but has remained fairly steady since our first market prediction back in April.

Here’s what the model has to say today…

The good news is that July will be the best month at the box office since December, 2019, with films released during the month earning a combined $700 million or so. Black Widow will almost certainly end up being one of the top 10 movies of 2021 at the box office, and its $80-million (theatrical) opening sets the new bar that future movies will be aiming for.

August is likely to see business quieten down again. The Suicide Squad will almost certainly be the highest earner for the month, and the model thinks it should open with around $64 million right now. Given the general uncertainty in the market, that gives it a realistic chance of beating Black Widow’s $80-million mark, and the increasing number of people returning to theaters means that the model thinks it should top $200 million in total.

The problem with August is that there isn’t much else coming out that looks likely to earn more than $100 million. September is a little better, thanks to Shang Chi and Venom: Let There Be Carnage, but October remains the month when it looks like we’ll be back to having a strong selection of movies coming to theaters. Dune has moved back a few weeks since we last did a market update, but is still coming out that month (more on one theory behind the slip in a moment).

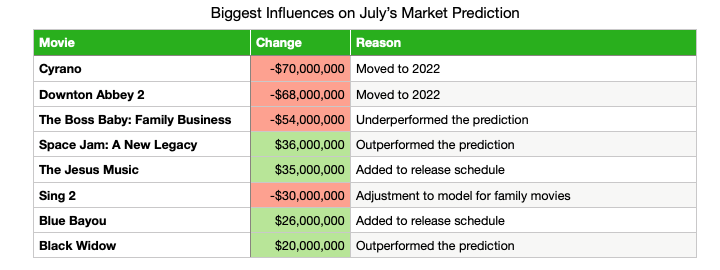

The biggest changes to the market prediction this month are due to a couple of movies that have been moved back into 2022: Cyrano and Downton Abbey 2. The model is quite bullish on both films’ chances, so moving them back hurts the box office projection for 2021 quite substantially.

The underperformance of The Boss Baby: Family Business had the biggest influence on the overall projection among movies that have come out in July. Family movies led the way during the early part of the pandemic recovery, with Tom and Jerry, Raya and the Last Dragon, and Cruella all performing well on opening weekend have enjoying long runs in theaters. Since then, that market segment has reverted much more closely to the overall average for all films. Spirit Untamed and Peter Rabbit 2 were also slightly disappointing. Hopefully the strong debut for Space Jam: A New Legacy is a harbinger of better things for movies aimed at a family audience. The model, however, has shifted its prediction for Sing 2 down again based on the recent performance of family films.

All in all, the market is recovering largely as the model expected. Our pandemic adjustment now stands at 51%, which is line with Morning Consult’s survey figure for the share of the population comfortable with going to theaters. I’ve added to the chart a new line that shows how the figures we’re measuring compare to the model’s assumption. (Click on the chart to go to Morning Consult’s page with more details on their survey):

If you’ll excuse me one moment of self-congratulation, the market is recovering very much in line with what I predicted back in April. The model’s predicted number has recently caught and slightly overtaken measures of actual activity though. If everything was going according to plan, about 59% of moviegoers would be back in theaters. The actual number looks to be around 51% right now. That difference of 8% isn’t vast, but it’s something I’ll be tracking closely over the next few weeks. The increase case counts in the US (and around the world) may be slowing down the recovery, and the “fourth wave” might cause reduced box office in the short term.

What exactly constitutes a “wave” is a matter for epidemiologists, and I won’t wade into that particular debate. Eyeballing the charts, however, suggests that a wave is likely to last at least a couple of months, and maybe longer. If we’re going into another wave, then we should expect to see adverse effects at the box office between now and mid-October (with fairly high uncertainty—it could be longer or shorter, and the latest wave might not substantially affect consumer behavior, depending on many factors that can’t really be predicted). Whether that explains the recent moving of Dune’s release date back from October 1 to October 22 I can’t say, but it’s one that I would support if I was in charge.

Our market prediction is based on the same model as the weekend predictions that we’ve been running since theaters started reopening towards the end of last year. We are now running the prediction model for every announced wide release on the release schedule and estimating the size of the market as a whole by assuming a relatively small amount of additional revenue from limited releases. The prediction for each movie is based on four factors:

The performance of similar films in recent years, and cast and crew Bankability. So far as possible, the model uses films in the same genre released by the same distributor as points of comparison. The predicted performance of franchise films is based on previous releases in the franchise. Cast and crew Bankability is weighted more heavily for non-franchise than for franchise films.

The current state of the theatrical market. We update our model after each weekend with a wide release to estimate what proportion of formerly-regular moviegoers are currently going to theaters. As of today, that figure is 51%. We also monitor Morning Consult’s weekly survey of moviegoers, and may make adjustments to our analysis if our number varies significantly from theirs.

Adjustments for specific genres. The pandemic has affected different segments of the audience in different ways. We are currently using four categories of movie in our model: “date night” films (which are doing worse than the general market), action movies (which are doing slightly better), family films, and “everything else” (which includes drama, comedy, and horror movies, among others). Family films seemed to be doing the best in the early stages of the recovery but are now performing much more like other genres.

The expected recovery of the theatrical market as the pandemic is brought under control. Once the market starts to recover, the model assumes it will take six months to reach a “new normal.” Growth will be slow at first, accelerate as more people become confident in going to theaters, and then slow down as more cautious moviegoers take time to return to attending. This is the classic ''S-shaped'' curve seen in economics textbooks (and in many cases in the real world). The model assumes that the market will settle back to 70% of its pre-pandemic size at the end of the recovery. (For more on this see my previous article, How quickly can the box office recover?) The model assumes that this recovery started on April 1, and will take until the beginning of October. Those parameters might be adjusted as the market situation evolves.

- Current release schedule

Bruce Nash, bruce.nash@the-numbers.com

-1-News.jpg)

Methodology

- Recent release schedule changes

- Subscribe to the Bankability Index for full details on our market predictions

Filed under: Marvel Cinematic Universe